Younger investors often ask me whether Exchange-Traded Funds (ETFs) are better than mutual funds and why I am not aggressively recommending them. I suspect this arises from their exposure to US markets, where ETFs are popular investment vehicles. While I have nothing against ETFs per se, there are several points that one should consider when investing in them.

First, let’s explore the similarities between ETFs and mutual funds. Both are pooled investment vehicles, meaning many people come together to contribute funds to an asset management company. The company employs a fund manager who oversees the funds and creates a portfolio for a fee.

Typically, in India, ETFs are passive funds. Mutual funds can be either active or passive, so the comparison arises only when investing in passive funds.

To recapitulate, passive funds are mutual funds or ETFs that track an index. As we know, a stock market index is made up of a specific group of stocks. The purpose is to measure the market’s direction and performance. Indexes are typically weighted averages of a group of stocks, with weights assigned based on preselected criteria, such as market capitalisation.

Companies move in and out of indexes if they fail to fulfill the criteria. It’s similar to a report card for the stock market. For example:

- Sensex shows how 30 top companies in India are doing. Nifty 50 shows how 50 big companies are doing.

If the index rises, it generally indicates that most of those companies are performing well.

If it declines, they’re not doing as well.

Why it matters:

- It tells you how the overall market is doing.

- It is used to compare the performance of your investments.

- It helps investors understand market trends easily.

A simple analogy is that there is a major cricket tournament with several countries competing against one another. Now, instead of tracking every player (which would be hundreds of stocks), the scoreboard shows how the top players of every country (like Sensex or Nifty companies) are performing.

The Sensex is like the score of the top 30 star players. The Nifty 50 is like the score of the top 50 players.

If your country’s score is increasing ➡️ the leading players (companies) are performing well.

If it’s decreasing ➡️ your team is not doing well.

So, we are circling back to passive funds or ETFs. They are constructed to exactly mimic the index they track. If Reliance accounts for 12.04% of the BSE Sensex, then it will represent the same percentage in the Index fund or ETF. Returns of a passive fund or a passive ETF should closely match the performance of that index. If your return is slightly lower, it’s referred to as the tracking error and is expected due to expenses, among other factors. However, if the performance is significantly lower than the index, there may be an issue with how it is being managed, and you might want to reconsider those funds or ETFs.

Looks like ETFs & Index funds behave exactly the same.. No, actually.

Differences are not in terms of the portfolio’s composition but in terms of operations. Suppose you invest in a Nifty 50 Index fund offered by an AMC. You will go to your intermediary or directly to the AMC and give them your investment. They will take your funds and allocate you units based on the Net Asset Value. This occurs once a day after the market closes. You will receive the end-of-day NAV, which will be your cost per unit of the fund.

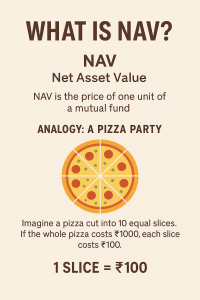

What is NAV or Net Asset Value?

It tells you the price of one unit of a mutual fund.

NAV = (Total value of mutual fund’s investments – expenses) ÷ total number of units.

If NAV goes up ➡️ your investment is growing.

If NAV goes down ➡️ the value of your fund has dropped.

The Pizza slice example is the most common one, but it does the job.

Imagine a group of 10 friends (investors) ordering a pizza (mutual fund).

The total cost of the pizza is ₹1,000, and it’s divided into 10 equal slices.

Each slice (NAV) = ₹1,000 ÷ 10 = ₹100

So, if you had joined the party and got a slice, you would pay ₹100.

Tomorrow, the pizza toppings will become fancier (fund value increases), and the pizza will be worth ₹1,200.

Each slice now = ₹1,200 ÷ 10 = ₹120 — the NAV has increased.

When you invest in an Index fund, you go to the AMC. They will give you the units at the end of the day and the cost, which is the declared NAV. When you wish to redeem, you return to the AMC, give them instructions, and they will return your funds. The funds you will get will be based on the declared NAV * the number of units you redeem.

I guess Index funds = ETFs?

When you invest in an index-based ETF, the subtle difference is that you buy and sell through a stockbroker, unlike going to the asset management company in the case of an index fund. When a retail investor wishes to buy or sell an ETF, the AMC does not allot or extinguish units, but, like shares, other investors satisfy that demand.

The ETF producer, which is typically an AMC, engages a market maker, or some entities may act spontaneously as one for profit. They maintain an inventory of the units and provide quotes for buying and selling them. As you can see, the price of stocks where buyers and sellers give bids and offers, there are two-way quotes for ETFs. The advantage is that you can buy or sell anytime during the day and not wait for the end of the day.

An ETF functions similarly to a mutual fund but is established once the initial investor’s contributions are used and traded on the market afterwards among investors. If a very large investor wants to invest in an ETF, they can go to the ETF producer, and the producer creates fresh units, but typically, the investment has to be in crores.

So, what is the issue?

The issue is that the quoted price may differ from the actual value of the ETF or the iNav. As explained above, the NAV represents the value of one unit of the Index fund or an ETF. Sometimes, the quoted price can be 2-3% higher than the iNAV. It can be much higher and will apply to buying and selling. Even with a lower expense ratio than a mutual fund, it may take years to make up for the higher cost in terms of returns.

The iNav is declared every 15/20 seconds for equity funds. You can check it on NSE/BSE sites and platforms like Zerodha, Groww, etc. When buying an ETF, ensure it is very close to the iNAV. The same goes for selling. If there isn’t enough liquidity in that ETF, there may be a large variance, and that’s not good for the investor. There are also additional brokerage costs that you need to pay for an ETF.

Hence, the resistance to ETFs.

Why are ETFs popular in the US & even here, many Institutional Investors prefer them?

In the US, there are differences in the tax treatment of gains in mutual funds vs ETFs. In India, there are none. Institutional investors in India possess substantial amounts to invest and create units at NAV from ETFs, preventing any price discrepancies. Mutual funds in India also have regulations requiring a minimum of 20 investors and prohibiting a single investor from holding more than 25% of a fund, a rule that does not apply to ETFs. As a result, they invest in ETFs for their own reasons. As markets deepen, there may be much more active trading in ETFs, liquidity will improve, and these price differential issues may get ironed out.

Index funds are my preferred choice over ETFs until that happens.

Neeta

Always a pleasure reading your articles Amita. They are super informative.

Amita

thankyou !