IPOs or investing in initial public offers of companies have started the cult of equity investing in India.

A privately-owned company offered ownership of its shares to Institutions and the general public for the first time.

The merchant bankers priced the shares offered to the public looking at the financial statements, and the demand they sensed for them. Typically they priced it attractively so that the lucky allottee of the share makes some gains when the company lists.

That’s how the IPO investor was born. There are investors who never buy on the exchange or the secondary market but only apply when the company comes to the market the first time with an initial public offer.

Retail investors apply in the initial public offering, get an allotment and then hold it for eternity and never sell. Before applying, they would just do a cursory vetting of the company, and if a broker or a friend would recommend, then mindlessly apply.

It was a relatively safe investment strategy as IPOs were priced attractively and post-listing gains were almost assured.

No longer is it this easy to make money.The game has changed.

Companies want to hit the markets when the sentiment is positive and there is a boom. They hire big gun bankers, create a lot of media hype and buzz about the companies. This ensures that they are able to sell their shares at a “premium”.

Institutions and high net worth investors borrow from banks at very low interest rates and make high-value applications.

Retail see the number of times the issue was oversubscribed and get excited. If they get an allotment they are ecstatic and wait for listing. Unfortunately, only about 50% of shares that come with an offer have a positive listing.

Sometimes when the listing is blockbuster, people jump in to buy hoping for future gains then they end up holding the bag.

As the veteran investor Warren Buffett says on IPO’s “It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller to a less-knowledgeable buyer”.

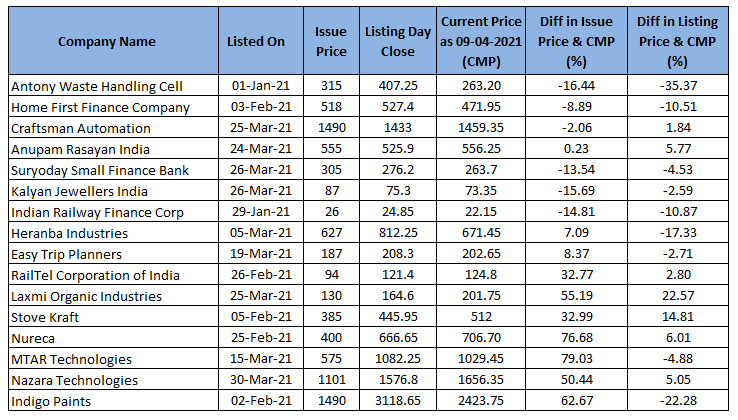

A look at some of the issues which hit the market in the calendar year 2021. While there is clearly an opportunity for gains, it is not a forgone conclusion. A little work gives you an idea of relative valuation and price helps in deciding to apply or not apply and later to buy or not from the secondary market.

As on 7/4/2021

Unless the investor does a bit of homework, the possibility of a loss cannot be ruled out. An initial Public offer means that this is a new company whose finances and track record of performance are not public.

And some companies are from industries and businesses which are unique so it is harder to price them correctly or forecast their profits. While this may be an opportunity or can be a threat. It makes a bit of sense to research a little about the IPO before writing a cheque.

It is hard enough to analyse the existing listed companies, let alone an IPO. Where to look, what to look for? Although it’s impossible to give a complete checklist you can begin with the draft red herring prospectus (DHRP) and red herring prospectus, (RHP).

These are filed with SEBI (the regulator) by the company which gives a wealth of information about the company. It’s a very long document running into hundreds of pages.

It is hard to go through all of it but some important financial information about the last three year’s sales, profit, loans, and details of the company can be studied.

Most brokers and advisors put up their analysis on their websites. You can ignore their recommendations but can look at the numbers which are presented in a concise manner.

I especially look at the legal / risk factors in the DHRP, the price-earnings of listed peers if any, and any other sharp, questionable practice by the promoters.

The resource which I look at is this site. It deals exclusively with IPOs and I get all the data I need in one place.

I don’t necessarily go by their recommendation to apply or not but it’s a good read to get their perspective as it is written simply.

The idea is to apply in companies with a good business model at a reasonably good price that can be held for the long term and not only for listing gains.

There isn’t an unlimited pool of funds available for everyone. Some investors do want to sell on listing and use the funds to apply in other IPO’s or trade with. Even if that’s the objective, you need to do some minimal homework so that if you end up with the stock long term, you are happy to own it if it doesn’t appreciate immediately.

Here are some factors to look out for:

- Consistency of Revenues

- The Price at which it is offered to the public is high. Now, what is high? It is a subjective definition. I look at the PE as compared to its listed peers and it should not be appalling.

- Size of the public issue & the purpose.

- If the company has a lot of litigations against it.

- If the management has given loans to Directors/Associate Companies.

It is better to refrain from investing if there is discomfort, even if the price may double or treble post listing of a few allegedly dubious companies which is a reality one has to live with.

For eg: The recently closed IPO of a company called Barbeque Nations.

The company offered shares via an IPO at a price of Rs. 500. They had done a private placement in January 2021 @ Rs 252 per share. This means the price it offered to some other investors a couple of months back was half of what is offered to the public.

The company is loss-making since 2019 & has made a huge loss of 100 Crs + for the first eight months of FY 2021.

Also with the Pandemic not yet conquered the turnaround may be at least a year away.

On the positive side, it’s a known brand with 167 restaurants and a presence in 3 countries. Also boasts of some marquee investors.

Even so, I gave it a pass. To prove the randomness of markets though, the company listed at a discount and then zoomed up and trading now at 700 +, with an appreciation of 40% +.

I found the price of IPO unjustified. If in the future, the company reports good performance happy to revisit.

Similarly.

The recently closed Macrotech Developers erstwhile Lodha Developers. In my opinion, Real Estate Developers tend to be opaque, the pandemic would have an impact on the sales, the performance of Macrotech has been inconsistent, so gave it a pass.

The mysteries of the market is worthy of a case for Sherlock Holmes to solve, Macrotech may very well list at a premium.

No FOMO there either.

Have also had very good gains in IPOs like IRCTC, Avenue Supermarkets, Gland Pharma to name a few.

The secret in markets is not to try and chase every trade there is and bet only on high conviction trades.

….

Sejal Goel

Good Read!